One Theme, Diverse Risks

Fusing the domain expertise of a specialist firm with the risk architecture of a generalist firm.

Introduction

Supermoon is the only venture fund purpose-built to back the full stack of sleep innovation. We invest across every industry that touches sleep: consumer, enterprise, medtech, diagnostics, biotech, therapeutics, hardware, software, and content — giving our LPs the diversification of a generalist fund with the edge of a focused sector specialist.

Risk Architecture

Excessive exposure to a single sector, geography, or asset increases risk. Diversification reduces risk.

Megafunds investing across sectors, geographies, and growth stages are inherently less risky than sector, geo, or stage-focused specialist funds. These specialist funds are riskier because their portfolio companies face the same risk factors: regulations, reimbursement decisions, market sentiments, procurement cycles, etc. A single storm can lay waste to an entire portfolio of businesses building in the same city. An entire portfolio banking with the same bank can create a single point of failure.

Our thematic focus on sleep is structurally different. While our portfolio companies share a theme — the science, technology, and sentiment of sleep — they do not share risk profiles.

Consider the breakdown of risks across our 20+ portfolio companies:

Medical device interventions (Aesyra, Restera) face FDA clearance timelines, clinical validation requirements, and physician adoption curves.

Medical device diagnostics (Bairitone Health) face risk factors similar to medtech interventions (FDA clearance, reimbursement coding and coverage decisions) but are also more exposed to clinical workflow adoption and standard-of-care risks.

Pharmaceutical and therapeutics companies (Mosanna Therapeutics) face clinical trial risk, IP risk, and eventual payer negotiations.

Prescription digital therapeutics (Big Health) sit at the intersection of clinical validation and enterprise health system sales and face their own distinct reimbursement and formulary access dynamics.

Consumer hardware companies (FreshBed, Amira, Loftie, Kimba) face manufacturing risk, retail distribution risk, and consumer discretionary spending sensitivity — an entirely different set of drivers from any of the clinical risks above.

Consumer brands and CPG (Future State, Ritual Brands) face stiffer competition, retail shelf dynamics, and marketing efficiency risks.

AI, software, and data platforms (EnsoData, Arcascope, Sahha, Arctop, Sleep AI) face B2B enterprise sales cycles, technical differentiation, and developer adoption risks.

Content and entertainment companies (Endel, Mind Candy, Athvance) face IP, distribution, and audience monetization risks.

Deep tech and incubation companies (Dust Systems) carry early-stage technical and commercial risks characteristic of frontier research.

A CMS reimbursement ruling that disrupts our diagnostics companies has no effect on Endel’s streaming revenue. A consumer discretionary spending contraction that weakens Loftie’s sales does not affect Big Health’s enterprise health system contracts. A formulation issue with Mosanna’s nasal spray does not affect Sahha’s B2B API business.

All of these businesses are “sleep” companies yet they are widely diversified across distinct, largely uncorrelated risk vectors.

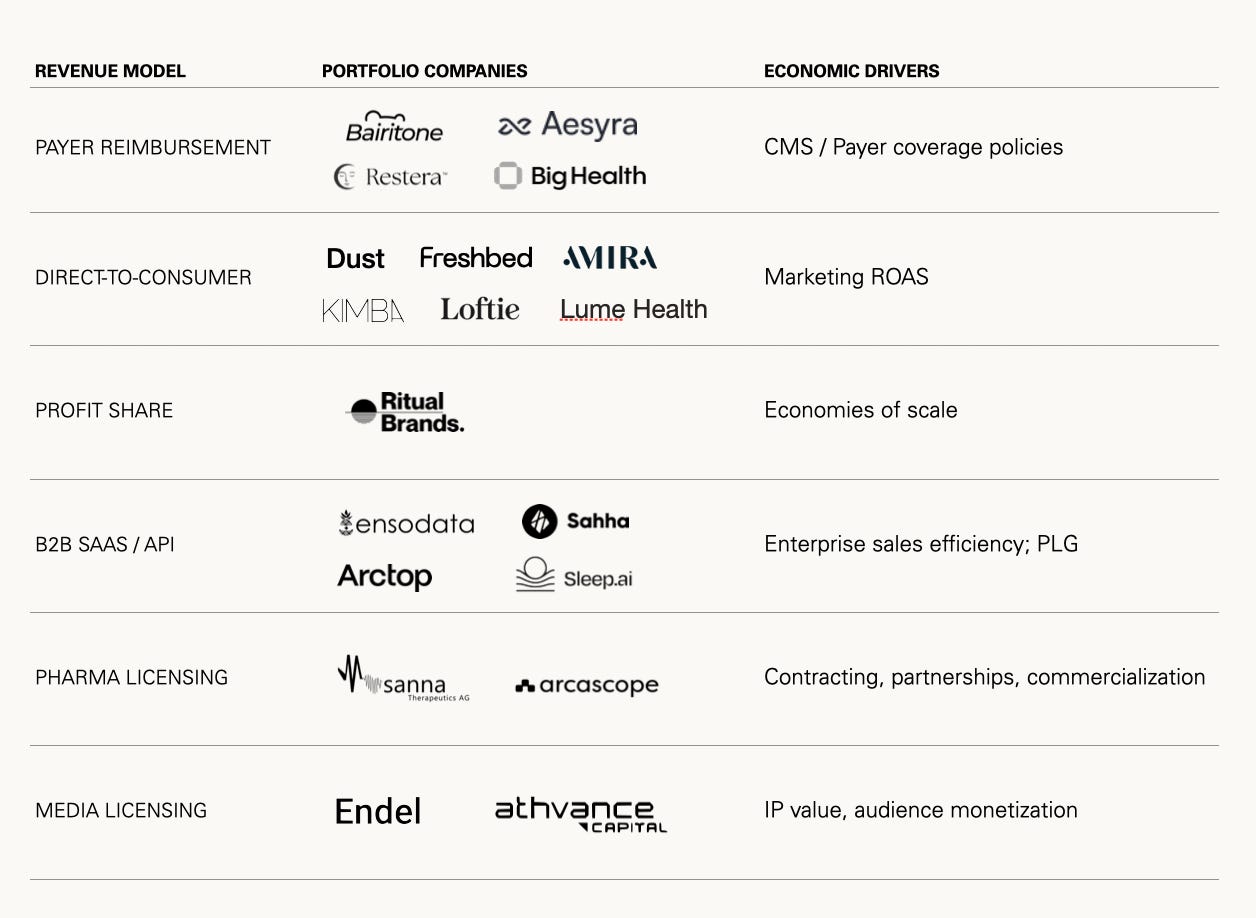

Revenue Model Diversity

How our companies generate revenue is as varied as how they manage risk. Distinct revenue architectures mean that macro shocks — interest rate cycles, consumer sentiment shifts, healthcare policy changes — hit different parts of the portfolio through entirely different transmission mechanisms:

These distinct revenue models diversify exposure to economic cycles.

Geographic Diversity

A less-discussed dimension of portfolio correlation is geography. Many specialist VCs inherit geographic concentration as a byproduct of specialist networks due to clustering of innovation around universities, incumbents, and startup communities. This creates single point-of-failure exposure. Natural disasters or regional conflict can disrupt an entire portfolio.

Fortunately for us, centers of sleep science excellence and innovation are distributed globally and our portfolio mirrors this broad distribution. Our portfolio companies span five different states and eight different countries, meaning that no single storm, war, or regional banking failure touches more than a small fraction of our portfolio.

Buyer Universe

Exit opportunity concentration also increases portfolio risk. A limited acquirer universe reduces optionality and number of potential bidders.

The broad range of categories and sectors featured across our portfolio maps to a diverse range of potential acquirers including Pharma/Biotech companies, Healthcare companies, Consumer/CPG companies, Media companies, Big Tech companies, Big Sleep companies, and PE firms.

No single acquirer category dominates.

Conclusion

No single scenario simultaneously impairs the full portfolio. In a downturn, our consumer businesses impacted by reduced discretionary spend would contract, our medtech & healthcare businesses would be less impacted, and cheaper digital therapeutics may perhaps accelerate. In an expansion, consumer brands and hardware may outperform while clinical-stage companies would continue to progress on their own timelines.

Supermoon is a research-driven VC that invests in scientists, technologists, and creatives building the future of sleep and sleep-adjacent categories. We invest globally in pre-seed to Series A stage businesses across enterprise, consumer, and biotech. If you’re building in sleep or are interested in partnering with one of our portfolio companies, I’d love to chat. You can reach me on LinkedIn and Twitter, or email me directly at gj@supermooncapital.com.

Looks like a great concentration of sleep knowledge!